You are here

Back to topFDK China Market Update — Week 16

April 21, 2025

This newsletter is published on behalf of Fruit Data Kings, a Berlin-based company specializing in pricing data and associated analytical tools for the fresh produce industry. For more information, visit the Fruit Data Kings website.

Apples (⇩)

New Zealand remains the primary supplier, accounting for nearly 80% of apple openings over the last three weeks. Royal Gala is dominating (40%), followed by NZ Queen (19%) and Dazzle (14%). NZ Royal Gala prices have firmed slightly to ¥259 (18 kg), trading 2% above last season’s average. NZ Dazzle has eased to ¥394 (18 kg), which is down 3% compared to last season. NZ Queen has experienced a notable decrease to ¥327 (18 kg), now 15% below its last-season average. South African Royal Gala has held steady around ¥224 (18 kg), trading 6% below last season. For further details, visit us online.

Grapes (⇩)

Chile (49%) and Australia (30%) are leading the grape supply, with Peru and India also contributing. Key varieties include Sweet Globe, Crimson and Red Globe. The overall price trend has been weaker. Peruvian Autumn Crisp has seen a significant drop to ¥194 (7.3 kg), trading 21% below last season. Chilean Red Globe has eased slightly to ¥176 (8.2 kg), although this is 17% above the 2023 season. Australian Crimson has softened marginally to ¥225 (9.5 kg), which is up 14% compared to the 2023 season but below last year’s value. Peruvian Sweet Globe has firmed to ¥239 (7.3 kg), while Australian Sweet Globe has also strengthened to ¥260 (9.5 kg) but remains 7% below 2023. Additional details are available online.

Nectarines (⇩)

Chilean nectarines continue as the exclusive source, with volumes declining sharply. Arctic Mist and Arctic Snow have been the primary varieties over the past three weeks. Arctic Snow prices have remained stable at ¥147 (9 kg), but this is 28% below last year. Arctic Mist has firmed slightly to ¥151 (9 kg), although this is also below last year’s value (−23%).

Oranges (⇩)

Orange volumes have increased, with Egypt strengthening its dominance. Valencia is the main variety. Egyptian Valencia prices have held steady around ¥143 (15 kg), maintaining a premium over last year (+13%) and the previous season (+8%). Visit us online for more details.

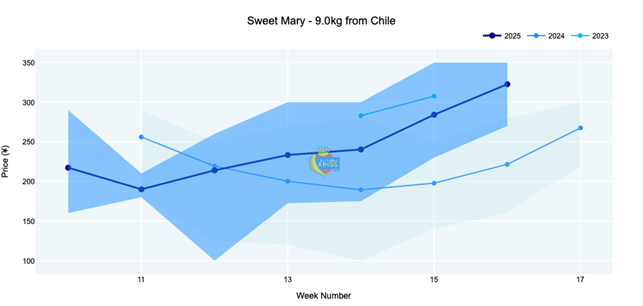

Plums (⇧)

Supply remains exclusively Chilean, although volumes have decreased substantially. Crimson Fall has dominated this week’s arrivals in southern China (49%). Pricing has strengthened considerably. Sweet Mary has climbed significantly to ¥309 (9 kg), 39% above last year. Crimson Fall has also firmed to ¥169 (9 kg), showing strong gains against last year (+28%) and holding steady compared to 2023.

Quick links:

Images: Pixabay (main image), Fruit Data Kings (body image)

Topics:

Regions:

-

April 21, 2025

-

April 21, 2025

-

April 17, 2025

-

April 15, 2025

-

April 14, 2025

-

April 08, 2025

-

March 23, 2025

-

April 06, 2025

-

March 27, 2025

-

March 24, 2025

Upcoming Events

Produce Marketplace

- Elangeni Food Group · South Africa

- Universal Capital Gr · Ecuador

- AGRI GATEX LIMITED · Africa

- Hainan ITG Logistics · A26,Haikou

- Joshua Lim · Malaysia

- City fresh fruit co. · Thailand

Add new comment